Is Social Security running out?

Does Social Security have a looming expiration date? Maybe. Maybe not. That really depends upon your point of view.

By late 2032, the trust fund built up for decades will officially be depleted, which could lead to an estimated 24% reduction in benefits if no legislative action is taken.1 For some, especially those who depend on Social Security as their main income, this reduction could have a meaningful impact on their financial security. But that’s not necessarily the whole story.

Is Social Security truly approaching insolvency?

Articles abound proclaiming that Social Security is on the verge of going the way of the dodo bird. Kaput. Goodbye. The end. And without action from our government, we will face the end of the trust fund as we know it in just six short years.

That's a scary thought for both those currently collecting retirement, and for the millions of workers hoping to collect their fair share in the future. But in reality, the hype is not only overstated, but there are also actions that you can take today—to help bridge the possible gap tomorrow.

Social Security’s humble beginnings and how it’s changed

The Social Security program has benefited millions of Americans for over seven decades. But are the program’s good intentions keeping pace with today’s demographics?

The Social Security Act of 1935 created the first permanent, nationwide old-age pension system, funded through contributions from both employers and employees.2 The system, dubbed Old-Age and Survivors Insurance (OASI) program, was created to provide economic security to the nation’s elderly. For over three decades Social Security accumulated a large reserve. During those years, the system collected more in payroll taxes than it paid out in benefits and expenses. However, that shifted in 2010 when it began paying out more money than it received.3 The trust fund is not a traditional cash reserve, but rather a collection of government securities used to help support benefit payments.

Am I paying for Social Security right now?

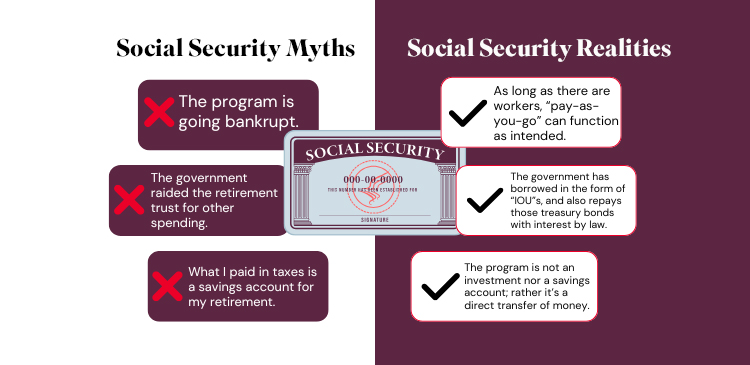

As it stands, Social Security remains the largest program in the U.S. budget, accounting for roughly one-fifth (about 21-22%) of federal spending.4 However, the government doesn’t save the 6.2 percent of your paycheck that goes into the Social Security fund, nor the matching portion that your employer contributes. If it were a true pay-as-you-go system, taxes collected from today’s workers directly fund today’s retirees.

Historically, there were always more workers than retirees, which allowed the Social Security program to build up reserves. However, as benefit payments began to exceed the money coming in, those reserves started to shrink—creating the potential income shortfall that future retirees may face.

The realities of Social Security solvency

Without government action, harsh realities are on deck for both current retirees as well as workers looking forward to a comfortable retirement. Because payroll taxes are the main source of Social Security funding, much of the crisis is largely due to the aging U.S. workforce. The ratio of workers to retirees has been steadily falling since 1950 when there were 16.5 workers for each beneficiary. Today, the ratio has plummeted to under three.5 The concern is real, as is the possibility that millions of retirees may fall victim to a Social Security funding shortfall in the decades to come.

The program is here to stay, but in what form?

While doom and gloom makes for eye-catching headlines, Social Security is in no danger of disappearing. And, proposed solutions abound, like:

- raising the full retirement age

- taxing greater income on more affluent earners

- privatizing savings for younger earners

- increasing payroll taxes

Congress could also simply change the law of the land at any time. None of these choices are easy. The good news is, so long as workers are paying payroll taxes, retirement benefits will continue. It’s the shape and form those benefits may take that remains an unknown.

What can I do in the face of Social Security’s uncertain future?

In truth, Social Security is not going "bankrupt.” But as previously mentioned, benefit cuts are a distinct possibility without congressional action. And that's something we all need to recognize. But short of government intervention, what can you do?

- Can you be more proactive and boost your IRA or 401(k) contributions?

- When do you plan to apply for Social Security? If you delay the start of Social Security benefits past what is considered the full retirement age, you can increase the amount you receive.

For current retirees, adjusting to Social Security cuts will likely prove more difficult to navigate. Life is only becoming more expensive, so try reducing your spending now to preserve more of your nest egg for the future.

For many, it may also make sense to withdraw from taxable accounts first so that your retirement savings can continue to grow and compound tax deferred.* Another option might be to return to work in a part-time capacity, again to reduce the money you need to withdraw from your savings, or even perhaps add to your savings. The key is to start considering your options now.

Consider an annuity as part of your retirement plan

Protecting your hard-earned income can be possible with proper planning. Annuities may provide what you need to help reduce your exposure to an unpredictable market, address your unique longevity concerns, leave a generous legacy and more. Plus, if you don’t need the income immediately, you can let it potentially grow tax deferred.

Work with a financial professional to put your retirement strategy into place

Social Security is not on the verge of going belly up, but like it or not, changes to the program are coming. Be sure to consult a trusted financial professional throughout your financial-planning process.

Your financial professional can:

- help you create a retirement strategy in line with today’s Social Security realities

- suggest a variety of approaches and products suited to your journey toward and during retirement

- provide answers for your specific circumstances

- walk you through our Social Security Calculator, which can help you decide when to begin collecting your Social Security benefits

Learn more about how an annuity from Jackson might fit into your retirement goals, and talk to a financial professional today.